Energy transition and security of supply

Contribution of the domestic extraction of natural resources to supply security considering Germany’s role in the international natural resource market

Latest Update: December 2025

Demand for natural resources

As an industrial and technology location, Germany is dependent on a secure supply of energy and non-energy (mineral) natural resources. Future technologies and projects such as the energy transition, electric mobility, digitalisation and decarbonisation of industry are changing the demand for certain natural resources. An increasing demand for natural resources such as lithium, rare earths, cobalt, nickel and copper is confirmed by regularly updated studies:

- International Energy Agency (IEA) – Global Critical Minerals Outlook 2024

- EU Commission – Supply chain analysis and material demand forecast in strategic technologies and sectors in the EU – A foresight study (2023)

- Federal Institute for Geosciences and Natural Resources (BGR) / DERA (German Raw Materials Agency) – Raw materials for future technologies (2021)

Basic pillars of the German supply of natural resources are domestic primary raw material extraction, the availability of secondary raw materials and raw material imports.1

Domestic primary raw materials

The demand for quarried natural resources (mainly for the building materials, glass and ceramics industries), potash products (for agriculture), rock salt (especially for the chemical and pharmaceutical industries as well as as as de-icing salt) and some industrial minerals can be met entirely from domestic natural resource sources. Individual energy resources such as lignite and natural gas as well as petroleum are also extracted close to consumption in Germany and contribute to the security of supply with natural resources (see also Which raw materials are extracted in Germany).2

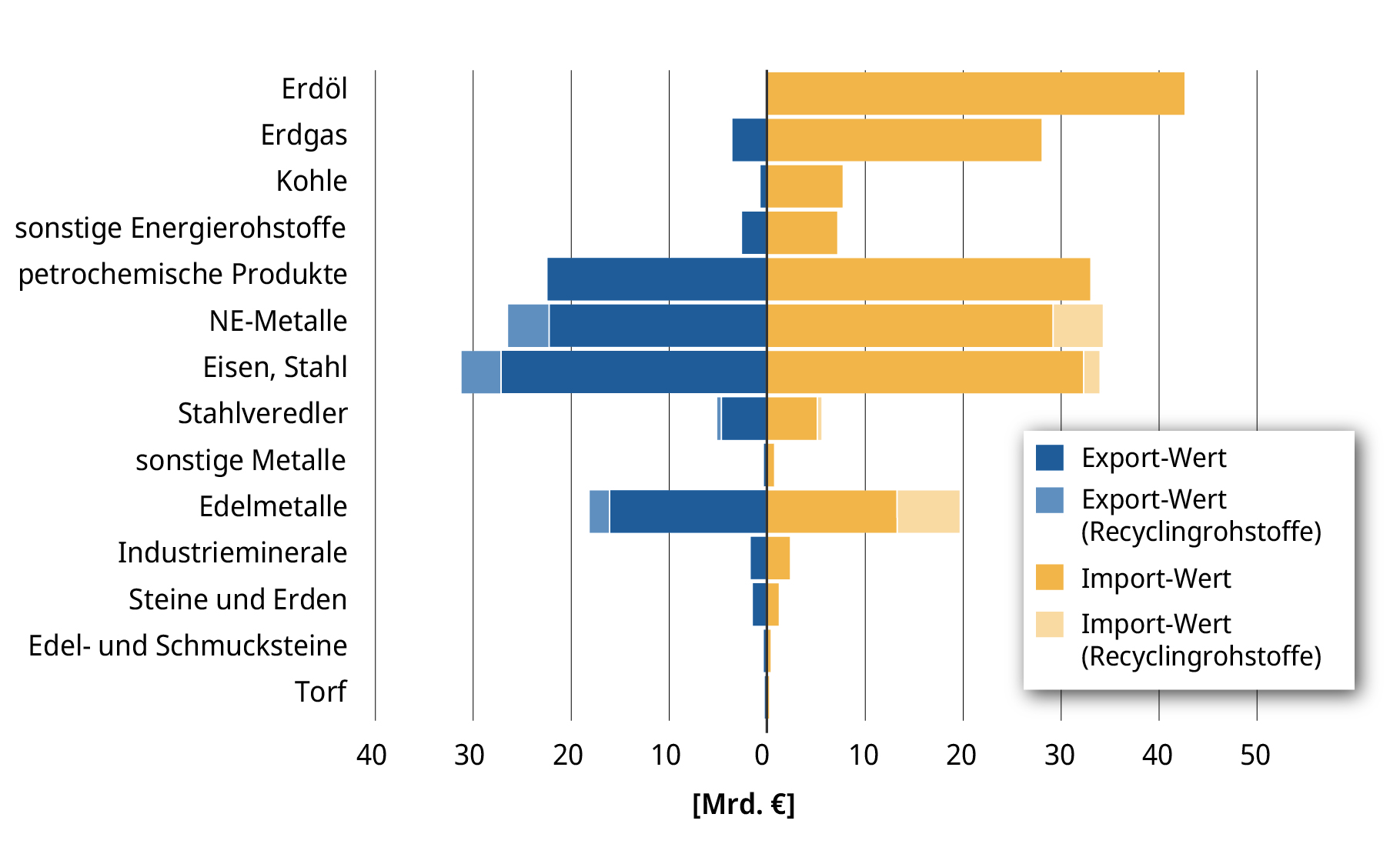

Mineral raw materials for future technologies are currently only produced in small quantities from mining in Germany. These include industrial minerals such as fluorite and barite, graphite, feldspar and coarse-grained quartz or quartz gravel for the production of silicon, but also lithium.3,4 Compared to other countries, high environmental and social standards apply to extraction. However, production is not sufficient to meet the demand for natural resources and other metals such as cobalt, nickel or rare earths are not extracted in Germany. This is also evident from the following graph on the foreign trade balance.

Figure 8: Foreign trade balance by value in 2023

Source: BGR – Bundesanstalt für Geowissenschaften und Rohstoffe [Federal Institute for Geosciences and Natural Resources] (2024) (see footnote 5)

Secondary raw materials from recycling

Some metallic natural resources, such as iron/steel, lead and aluminium, are often not consumed but used due to their good recyclability. They can be returned to a product cycle after processing, although this recycling process does not function endlessly and is energy-intensive due to the loss of material. Many products made from non-metallic raw materials, on the other hand, are often chemically modified (e.g. cement, concrete) and therefore cannot be returned directly to the product cycle. However, some can be recycled as substitutes (e.g. building materials) for primary raw materials (recycled or secondary raw materials).

Secondary raw materials contribute to the domestic supply of raw materials and reduce import dependency. For example, aluminium is on the list of strategic raw materials of the Critical Raw Materials Act (CRMA), a European regulation on critical and strategic raw materials that requires, among other things, an increase in processing and recycling capacities in the EU. In 2023, around 2,976,000 tonnes of aluminium were produced in Germany, for which 2,786,000 tonnes of aluminium were recycled.6 The share of secondary raw materials (steel and iron scrap) in steel production was around 42% in 2023.7

This is not the case, for example, with lithium, which is also one of the strategic raw materials on the CRMA list and is mainly contained in batteries. Recycling processes for lithium are technically complex processes8 and lithium recycling of batteries currently takes place only to a small extent. It is expected that lithium demand will rise sharply in the coming years, and in addition to the primary supply, the secondary sector will play an increasingly important role in the future for the overall supply. Many batteries from electric vehicles are estimated to reach the end of their life9 in 8-10 years and are only then available for recycling.10 To strengthen the circular economy, the Federal Government has adopted the National Circular Economy Strategy (NKWS) 2024 (see Circular economy, in particular recycling).

The goal specified therein is to reduce the critical import dependencies on raw materials, strengthen the circular economy and reduce the overall consumption of raw materials in order to achieve a resilient, sustainable supply of raw materials. Successful implementation requires a rethink of industrial and innovation policy at the various international levels, as well as in Germany. This includes the targeted promotion of material-efficient approaches to the absolute reduction of the use of raw materials in industrial production (e.g. lightweight construction taking into account recyclability), of ecodesign approaches (e.g. improving the durability, reusability and repairability of products) and of approaches to the substitution of non-renewable, scarce or critical raw materials (see also Circular economy, in particular recycling). Securing high-quality secondary raw materials from the recycling processes for the economic cycle is a factor for increased use. The right economic and environmental incentives must be put in place to ensure that our raw material supply is responsible and secure in the future.

However, the supply of recycled materials is not sufficient to fully compensate for the rising demand for raw materials for the transformation of energy supply and for other future technologies. In view of the geopolitical developments and the challenges mentioned in relation to the import of raw materials, the Federal Government sees the need to strengthen diversification in the supply chains of critical and strategic raw materials as well as domestic raw material extraction in cooperation with companies in the medium and long term.

Natural resource impports

In the case of metals, individual industrial minerals and energy raw materials (with the exception of lignite), the industry is heavily dependent on imports from outside Europe and thus on the availability on the international raw material markets. At 298.4 million tonnes, Germany imported almost 13% less raw materials in 2023 than in the previous year. Imports of energy raw materials (-15.1%), non-metals (-8.9%) and metals (-6.9%) declined significantly. In 2023, energy raw materials, metals and non-metals (of which about 57% are industrial minerals) worth €216.2 billion were imported into Germany.11 Further information on import volumes in the D-EITI sectors of German raw material extraction (petroleum and gas, lignite and hard coal, salts, stones/earths, industrial minerals, iron ore) can be found under the topic The extractive industry in Germany.

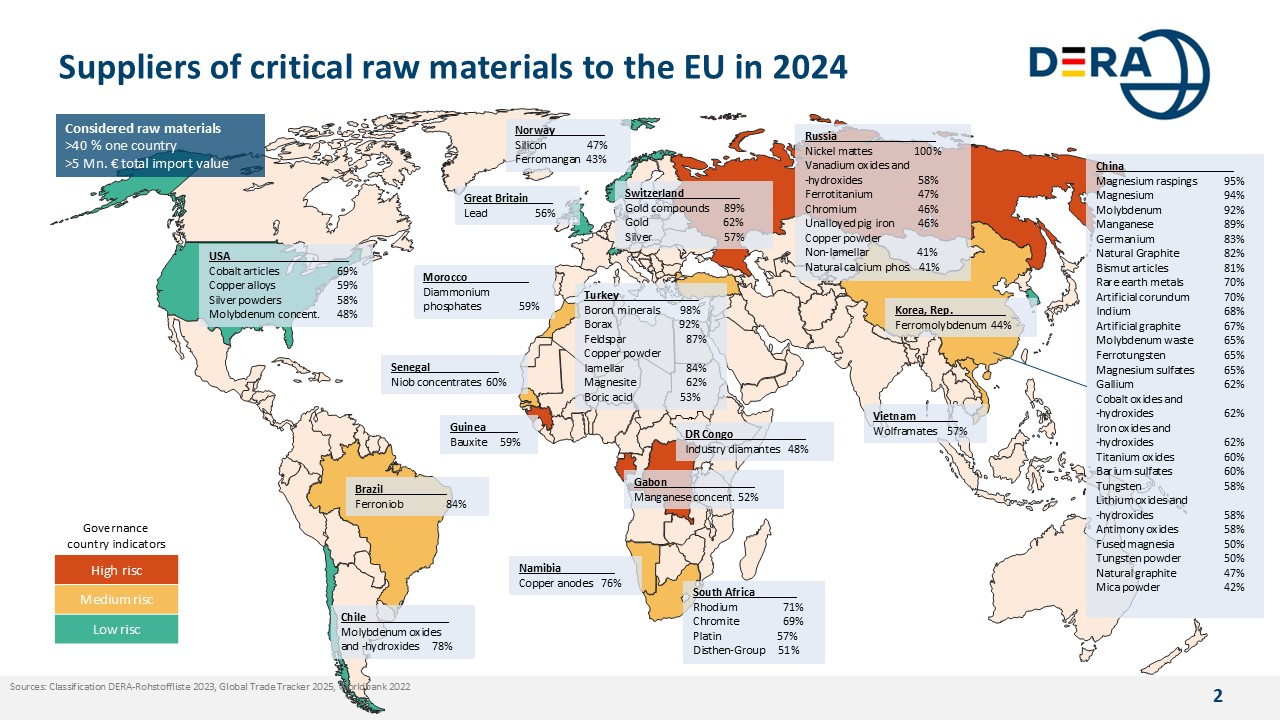

The world map (Figure 10) shows the most important supplier countries of the EU in 2023 of 60 potentially critically categorised mining, refining and commercial products (see DERA list of raw materials 202312), of which more than 40% come from one country and had a total trade value of more than 5 million euros in 2023.13 The BGR report “Germany – Raw Materials Situation”14 publishes annual data on German imports of the most important critical and strategic raw materials. A complete list of these imports can be found at Destatis.15 It should be noted that a significant proportion of raw materials is imported via EU countries, but these are only intermediate stations in the raw materials trade.

Figure 9: EU import dependency on critical raw materials in 202316

Source: DERA – from Chart of the Month, August 2023 (updated for the year 2023)

Therefore, an examination of Germany’s import dependency from the perspective of the German import figures is only partially meaningful. The degree of diversification of raw material imports on the EU internal market in Graph 9 also illustrates Germany’s dependence on imports.

{acf_content_section_2}

{acf_content_section_3}

Sources

{acf_quellenangaben}